|

Saturday 1st July 2017

Hi Friend,

Cyclical Buffers ... The Bank of England Makes a Move ...

|

|  |

In the US growth was upgraded to 2% year on year in the first quarter, according to the latest data from the Bureau of Economic Accounts. Janet Yellen remains committed to further rate increases despite the moderation in inflation. The Fed chief is confident about recovery, “Would I say there will never, ever be another financial crisis? That would be going too far, but I do think we are much safer, and I hope that it will not be in our lifetimes and I don’t believe it will be.”

So peace in our time and no financial crisis in our lifetime. It's a brave call especially with Trump in the White House. Perhaps the cyclical buffers are the key to financial stability. This week the ONS confirmed growth in the UK was 2% in the first quarter. The Governor admitted an increase in rates was possible, if investment recovered to offset the strength of consumer spending. Strong growth in manufacturing (2.5%) and construction (2.8%) supported private service sector growth over 2.5%. Consumer spending was up by 2.6%, business investment was up by just 0.7%. Still much to be done with investment. Perhaps the next rate rise will be delayed into 2018 after all.

The Financial Policy Committee voted to increase the counter cyclical buffer (CCyB) to 0.5% with a further rise to 1.0% expected in November. The FPC is concerned about the growth in consumer credit. Mortages, credit cards and car finance featured. The buffer has merely returned to the level before the ill judged reduction in August. CCyB has been restored but why not base rates? The Bank isn't really concerned about current levels of debt or about car finance particularly. The impact levels on bank assets are less then 0.1% assuming car prices fell by 30% and every one handed back the keys. The band with for the CCyB is 0.0% to 2.5% within the cycle. Currently, the CCyB tightening is 20% achieved. A comparative level for base rates would be 1.0% assuming rate normalization of 4.5%. So why the inconsistency?

Increasing the cyclical buffer with base rates on hold is trimming the sails with engines at full steam ahead. Consumer spending in current terms was up by 4.6% in the first quarter. Imports were up by 6% as the trade deficit continues to deteriorate. Cyclical buffers or monetary duffers ... concerns about consumer borrowing convince the markets, rates are set to rise ...

|

|  |

In other economic news ...

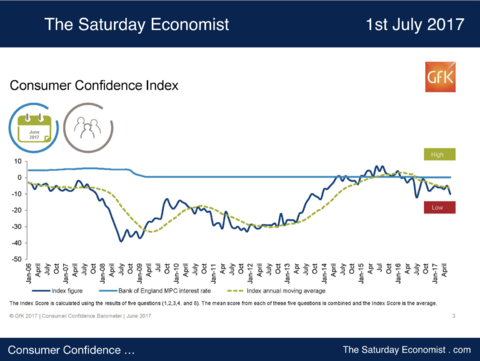

Consumer confidence took a dive in the latest data from GfK. Concerns about household finances appeared to hit spending intentions in the months ahead. Higher inflation and flat earnings are squeezing household incomes according to the official data. The impact on sentiment post election is apparent but may be short lived.

The savings ratio plummeted to 1.7% in the first quarter of the year. It hasn't been so low since records began in the early sixties. Averaging over 5% last year, the overall average since 2008 has been 8%. The data must be subject to revision in the months ahead.

Car output dropped by 9.7% in May according to the SMMT. May was a particularly strong month last year. The year to date output is up by 1%. Strong demand for exports offset the weakness in domestic sales. Exports account for 80% of total output, with a large proportion destined for the EU. Further growth is expected this year as new models come on stream but the overall growth in the year will be muted.

So what does this all mean for growth? In the US we have increased our forecasts for the year to 2.4%. In the UK, the consensus is for growth of just 1.6%. We expect the growth to continue around the 2% plus rate despite uncertainty about a hung parliament and the EU talks ...

|

| West Wing WTF ...

Mika Brzezinski the tweet too far ...

Morning Joe became the story of the week in the White House as President Trump lashed out at Morning Joe and Mika Brzezinski particularly. Abusive, sexist and outrageous the condemnation from media and within Congress from both sides of the house continued.

Trump lashed out at "Psycho Joe" and "Low I.Q Crazy Mika". The MSNBC hosts were moderate in their response.

"America's leaders and allies are asking themselves yet again whether this man is fit to be president. We have our doubts but we are both certain the man is not mentally equipped to continue watching our show, "Morning Joe".

In the White House, Deputy Press Secretary Sarah Huckabee Sanders told reporters. "The American people elected a fighter, they knew what they were getting when the voted for Trump". Yep now we are all beginning to realise ...

That's all for this week from The West Wing, Whisky, Tango, Foxtrot ... You can check out the series of blog posts here or leave any comments or LIKES on the Facebook page here ...

|

| | |

The week in markets ...

Markets fell, bond yields increased. The Dollar fell against the Euro and the Pound. Sterling tested the $1.30 level. Gold fell and oil prices rallied slightly ... central banks are moving slowly in the UK and Europe as the Fed sets the pace ...

|

| John

That's

all for this week. Have a great week-end ...

|

| | © 2017 John Ashcroft, Economics, Strategy and Social Media, experience worth sharing.

______________________________________________________________________________________________________________

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of advice relating to finance or investment.

______________________________________________________________________________________________________________

If you do not wish to receive any further Saturday Economist updates, please unsubscribe using the buttons below or drop me an email at jkaonline@me.com. If you enjoy the content, why not forward to a friend, they can sign up here ...

_______________________________________________________________________________________

For details of our Privacy Policy and our Terms and Conditions check out our main web site. John Ashcroft and Company.com

_______________________________________________________________________________________________________________

Copyright © 2017 The Saturday Economist, All rights reserved. You are receiving this email as a member of the Saturday Economist Mailing List or the Dimensions of Strategy List. You may have joined the list from Linkedin, Facebook Google+ or one of the related web sites. Our mailing address is: The Saturday Economist, Tower 12, Spinningfields, Manchester, M3 3BZ, United Kingdom.

|

| |

|

|